All Categories

Featured

Table of Contents

Different policies have various optimum levels for the quantity you can spend, up to 100%., is added to the cash money value of the policy if the indexed account shows gains (generally computed over a month).

This suggests $200 is included to the money value (4% 50% $10,000 = $200). If the index drops in worth or continues to be consistent, the account nets little or absolutely nothing. But there's one advantage: the insurance policy holder is secured from sustaining losses. They do like safeties, IULs are not taken into consideration financial investment safety and securities.

Having this implies the existing cash money worth is shielded from losses in an inadequately performing market. "If the index creates a adverse return, the customer does not get involved in an adverse attributing price," Niefeld said. Simply put, the account will certainly not lose its initial cash worth. The cash money worth builds up tax obligation deferred, and the survivor benefit is tax-free for recipients.

Iul Tax Free

A person that develops the plan over a time when the market is executing inadequately can finish up with high premium repayments that do not add at all to the money value. The plan might after that possibly gap if the costs repayments aren't made on schedule later in life, which can negate the factor of life insurance policy completely.

Boosts in the cash money value are restricted by the insurer. Insurer often establish optimal involvement prices of less than 100%. Furthermore, returns on equity (ROE) indexes are often topped at particular amounts during good years. These limitations can limit the real price of return that's credited toward your account yearly, regardless of just how well the plan's hidden index does.

The insurer makes cash by maintaining a section of the gains, including anything over the cap.

The potential for a higher price of return is one benefit to IUL insurance policies contrasted to other life insurance coverage plans. Returns can in reality be reduced than returns on various other items, depending on how the market does.

In the event of plan termination, gains become taxed as revenue. Charges are normally front-loaded and constructed right into complex attributing rate estimations, which might perplex some investors.

In many cases, taking a partial withdrawal will likewise completely reduce the survivor benefit. Terminating or surrendering a plan can lead to more prices. Because instance, the money surrender worth might be less than the collective costs paid. Pros Supply greater returns than various other life insurance policy plans Allows tax-free funding gains IUL does not reduce Social Safety advantages Plans can be made around your threat appetite Cons Returns covered at a specific level No ensured returns IUL may have greater fees than various other plans Unlike other kinds of life insurance policy, the worth of an IUL insurance plan is tied to an index connected to the securities market.

Online Universal Life Insurance Quotes

There are many various other kinds of life insurance policies, clarified below. Term life insurance coverage provides a set advantage if the insurance holder passes away within a set time period, generally 10 to three decades. This is one of one of the most economical sorts of life insurance policy, in addition to the most basic, though there's no cash money worth build-up.

The policy acquires value according to a repaired schedule, and there are fewer costs than an IUL insurance coverage policy. Variable life insurance comes with even more versatility than IUL insurance coverage, implying that it is likewise much more difficult.

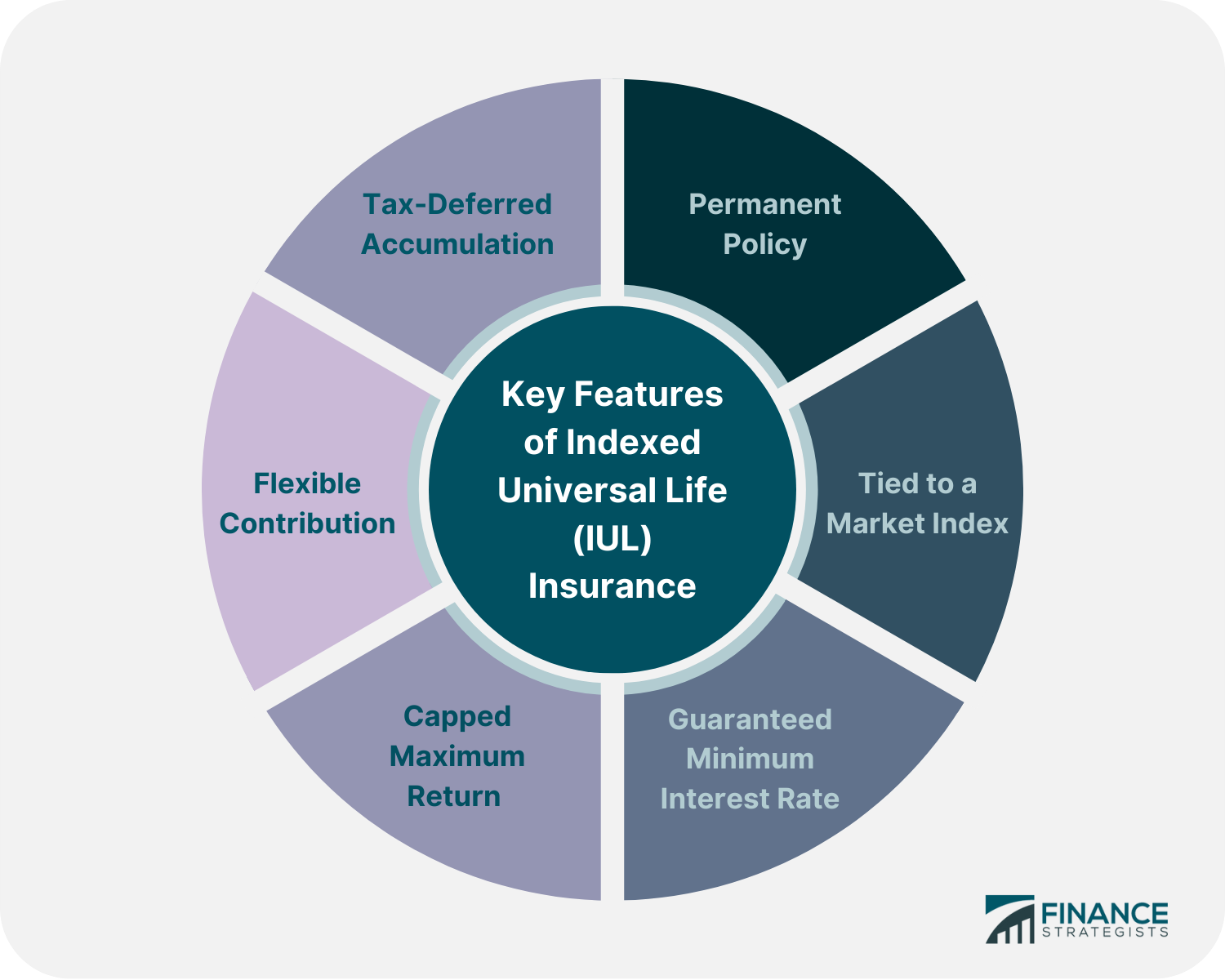

An IUL plan can offer you with the very same kind of insurance coverage security that a irreversible life insurance policy policy does. Remember, this kind of insurance policy continues to be undamaged throughout your whole life similar to other long-term life insurance policy plans. It also allows you to construct cash value as you age with a stock exchange index account.

Indexed Universal Life Insurance Good Or Bad

Remember, though, that if there's anything you're uncertain of or you're on the fence concerning obtaining any kind of type of insurance policy, be certain to speak with a professional. This way you'll understand if it's inexpensive and whether it matches your economic strategy. The expense of an indexed global life plan relies on numerous aspects.

You will certainly lose the death benefit named in the policy. On the other hand, an IUL comes with a death advantage and an additional money value that the insurance holder can borrow versus.

Indexed universal life insurance policy can help you fulfill your household's requirements for financial defense while also constructing cash worth. These policies can be a lot more intricate contrasted to other types of life insurance coverage, and they aren't always right for every investor. Speaking with a knowledgeable life insurance coverage agent or broker can assist you choose if indexed universal life insurance policy is a great suitable for you.

No matter just how well you intend for the future, there are occasions in life, both anticipated and unforeseen, that can influence the monetary well-being of you and your loved ones. That's a factor for life insurance coverage.

Points like prospective tax increases, inflation, financial emergencies, and preparing for events like university, retirement, or perhaps weddings. Some kinds of life insurance policy can assist with these and other worries too, such as indexed global life insurance coverage, or merely IUL. With IUL, your policy can be a funds, because it has the possible to build value with time.

An index might affect your rate of interest credited, you can not spend or directly participate in an index. Here, your plan tracks, however is not really spent in, an external market index like the S&P 500 Index.

Term Insurance Vs Universal Life

Fees and costs might lower plan worths. This passion is secured in. If the market goes down, you will not shed any kind of rate of interest due to the drop. You can additionally select to receive fixed passion, one collection predictable rates of interest month after month, despite the market. Due to the fact that no solitary allotment will certainly be most efficient in all market environments, your monetary expert can assist you establish which combination might fit your monetary objectives.

That leaves much more in your plan to potentially maintain growing over time. Down the roadway, you can access any available money worth with plan car loans or withdrawals.

Talk to your economic expert regarding how an indexed universal life insurance policy plan might be component of your total monetary technique. This content is for general educational objectives just. It is not meant to give fiduciary, tax obligation, or lawful suggestions and can not be made use of to avoid tax obligation fines; nor is it intended to market, advertise, or recommend any type of tax plan or setup.

What Is Universal Life Insurance Vs Term

In the occasion of a gap, exceptional plan finances over of unrecovered expense basis will certainly be subject to normal income tax obligation. If a plan is a changed endowment agreement (MEC), plan loans and withdrawals will be taxed as regular revenue to the extent there are profits in the policy.

Some indexes have numerous variations that can weight elements or might track the effect of rewards in a different way. An index may impact your rate of interest attributed, you can not get, directly participate in or receive reward repayments from any of them with the policy Although an external market index might influence your passion attributed, your plan does not straight get involved in any supply or equity or bond investments.

This web content does not use in the state of New York. Guarantees are backed by the economic toughness and claims-paying capability of Allianz Life insurance policy Company of North America. Products are released by Allianz Life insurance policy Firm of The United States And Canada, 5701 Golden Hills Drive, Minneapolis, MN 55416-1297. .

Iul Life Insurance Vs Whole Life

The information and descriptions consisted of here are not planned to be complete summaries of all terms, problems and exclusions applicable to the product or services. The precise insurance policy protection under any type of nation Investors insurance coverage item is subject to the terms, conditions and exemptions in the real plans as released. Products and services described in this internet site differ from one state to another and not all items, coverages or services are readily available in all states.

Your current browser may restrict that experience. You might be making use of an old internet browser that's in need of support, or settings within your browser that are not suitable with our website.

New York Life Indexed Universal Life Insurance

Already making use of an upgraded browser and still having problem? Please offer us a telephone call at for additional help. Your current internet browser: Finding ...

{kind=link}

Table of Contents

Latest Posts

指数 型 保险

Best Variable Life Insurance

Universal Life Crediting Rate

More

Latest Posts

指数 型 保险

Best Variable Life Insurance

Universal Life Crediting Rate